Net Present Value Formula for Innovation: When NPV Works (and Fails)

It's not a Magic 8-Ball, but it's not magic either.

By Tristan Kromer·

By Tristan Kromer·Quick Answer: The net present value formula can be used for innovation projects, but not on its own — it requires high confidence in projected cash flows, which early-stage innovations rarely have. Instead of treating NPV as a standalone decision tool, we can integrate it into a Monte Carlo simulation that uses estimated ranges for every variable, producing a probability distribution of NPV outcomes rather than a single misleading number. This lets us make informed Pivot-or-Persevere decisions while honestly accounting for uncertainty.

By Tristan Kromer I recently received a question about our Innovation Accounting Program that I’ve heard a couple of times now, and it deserves an answer:

“…is there somewhere in this program they show you NPV? (net present value calculations and how the innovation accounting is different from NPV?)”

It’s a great question, so let’s dig into it. First off…

What is a Net Present Value formula (NPV)?

(This is a bit of a long explanation, so if you already know what an NPV formula is, skip to Why Shouldn’t You Use NPV for Innovation Projects?) The Net Present Value formula is a standard metric taught in most business schools and finance classes, and is used to make a decision on an investment. Basically, if the NPV is greater than zero, you should make the investment. If it’s below zero, you should not. NPV does this by collapsing a timeline of revenue and expenses into a single, discrete number that includes the opportunity cost of putting your money elsewhere. It’s like magic! It makes complex decisions easy. Or is it more like a Magic 8-Ball, and arbitrary?

(This is a bit of a long explanation, so if you already know what an NPV formula is, skip to Why Shouldn’t You Use NPV for Innovation Projects?) The Net Present Value formula is a standard metric taught in most business schools and finance classes, and is used to make a decision on an investment. Basically, if the NPV is greater than zero, you should make the investment. If it’s below zero, you should not. NPV does this by collapsing a timeline of revenue and expenses into a single, discrete number that includes the opportunity cost of putting your money elsewhere. It’s like magic! It makes complex decisions easy. Or is it more like a Magic 8-Ball, and arbitrary?  Well, it’s a bit of both. But when it’s used correctly, NPV can be a powerful tool. So you need to understand what goes into an NPV calculation before you can use it effectively for an innovation project.

Well, it’s a bit of both. But when it’s used correctly, NPV can be a powerful tool. So you need to understand what goes into an NPV calculation before you can use it effectively for an innovation project.

Example: The NPV of a food truck

Imagine you are starting a food truck business. You expect to make $1 million per year, and it will cost you $1 million to start the food truck. Is this a good investment? Well, on the surface, it’s break-even. I spend one million to earn one million. So there’s no profit, but I also don’t lose any money.

Imagine you are starting a food truck business. You expect to make $1 million per year, and it will cost you $1 million to start the food truck. Is this a good investment? Well, on the surface, it’s break-even. I spend one million to earn one million. So there’s no profit, but I also don’t lose any money.  If the profit was $1 million and one dollar, it would suddenly be profitable. But should I still make the investment?

If the profit was $1 million and one dollar, it would suddenly be profitable. But should I still make the investment?  The Net Present Value formula says NO. This is because of the opportunity cost. There are a LOT of other things I could do with $1 million dollars. At worst, I could put my million dollars in the bank at a 5% interest rate and I would end the year with $1,050,000 – a profit of $50,000. Since $50,000 is better than $1, I should put my money in the bank instead of investing in a food truck. This is what economists call the time value of money. Put simply, a dollar now is better than a dollar later because you can invest that dollar now and earn more money later.

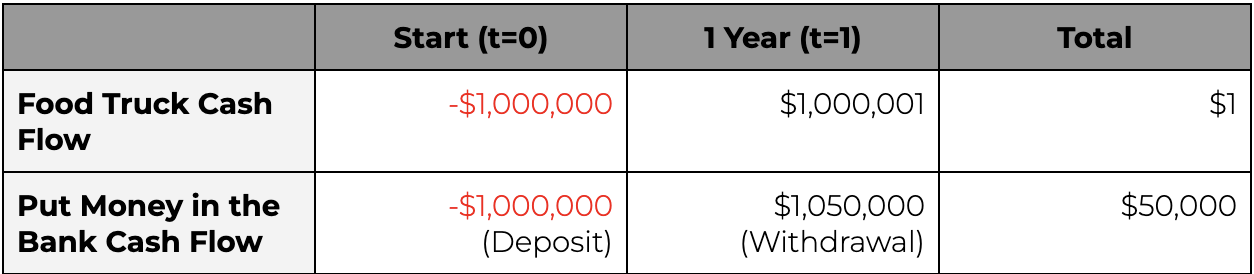

The Net Present Value formula says NO. This is because of the opportunity cost. There are a LOT of other things I could do with $1 million dollars. At worst, I could put my million dollars in the bank at a 5% interest rate and I would end the year with $1,050,000 – a profit of $50,000. Since $50,000 is better than $1, I should put my money in the bank instead of investing in a food truck. This is what economists call the time value of money. Put simply, a dollar now is better than a dollar later because you can invest that dollar now and earn more money later.  The NPV formula is basically a way of making that same comparison. But instead of calculating how much money we might make in two alternative investments at some arbitrary point in the future, NPV allows us to calculate the value of “future money” in “today’s dollars.” In other words, if we use the NPV calculation, we would find that $1 million in revenue next year is worth ~$952,380.95 today. This is because 5% interest on $952,380.95 is $47,619.05. So $47,619.05 + $952,380.95 = $1,000,000. Here’s the Present Value for the food truck in each time period compared with the actual cash values.

The NPV formula is basically a way of making that same comparison. But instead of calculating how much money we might make in two alternative investments at some arbitrary point in the future, NPV allows us to calculate the value of “future money” in “today’s dollars.” In other words, if we use the NPV calculation, we would find that $1 million in revenue next year is worth ~$952,380.95 today. This is because 5% interest on $952,380.95 is $47,619.05. So $47,619.05 + $952,380.95 = $1,000,000. Here’s the Present Value for the food truck in each time period compared with the actual cash values.  Essentially, the food truck loses us money because we are missing out on the opportunity to earn money in the bank. (And we’re not even talking about the risk involved in starting a food truck yet. More on that below.) Would you invest $1 million to receive $952,381.43 in return?

Essentially, the food truck loses us money because we are missing out on the opportunity to earn money in the bank. (And we’re not even talking about the risk involved in starting a food truck yet. More on that below.) Would you invest $1 million to receive $952,381.43 in return?

How do you use the NPV?

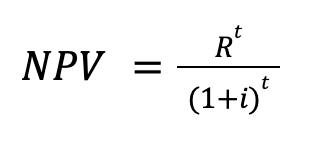

Don’t panic, but here’s the formula:  Let’s translate the terms:

Let’s translate the terms:

NPV = Net Present Value

The formula for NPV is so commonly used in financial analysis that it’s baked into Excel as “=NPV(rate,value1,,…)”. So it’s not actually hard to use or calculate.

Rt = Net cash flow at a given point in time “t”

This means that we’re going to perform this calculation on every single predicted cash inflow or outflow to the business (just like with the Excel formula). We’ll perform this calculation on every time period with every profit and loss from our investment.

t = Time of the cash flow

This is just referencing the time period again. We’ll make this calculation for each cash inflow at each point in time and add them all together.

i = Discount rate

This is a specific rate that represents the opportunity costs of putting your money into this specific investment. In other words, as an alternative to this investment, you could put the money into a safe, low-risk savings account and earn 5% interest. So if this food truck earns less than 5% return on your investment, it’s better to put your money in the bank.

Why shouldn’t you use NPV for innovation projects?

Unfortunately, you can only use the Net Present Value formula effectively if you know all the cash inflows and outflows and the discount rate. In other words, you must have extreme confidence in the numbers or you get a “garbage in, garbage out” calculation that is basically meaningless. If you have any uncertainty in your financial model, then the Net Present Value formula just represents a set of assumptions dressed up to look like something more precise and scientific than it actually is. Your revenue in Year 4 could be $1M or it could be $137.57. Your costs could be $2 per unit or $8 per unit. The cost of capital could be 1% or 10%. In essence, the NPV calculation just adds one more assumption (the discount rate) into the decision.

How you can use NPV for innovation projects

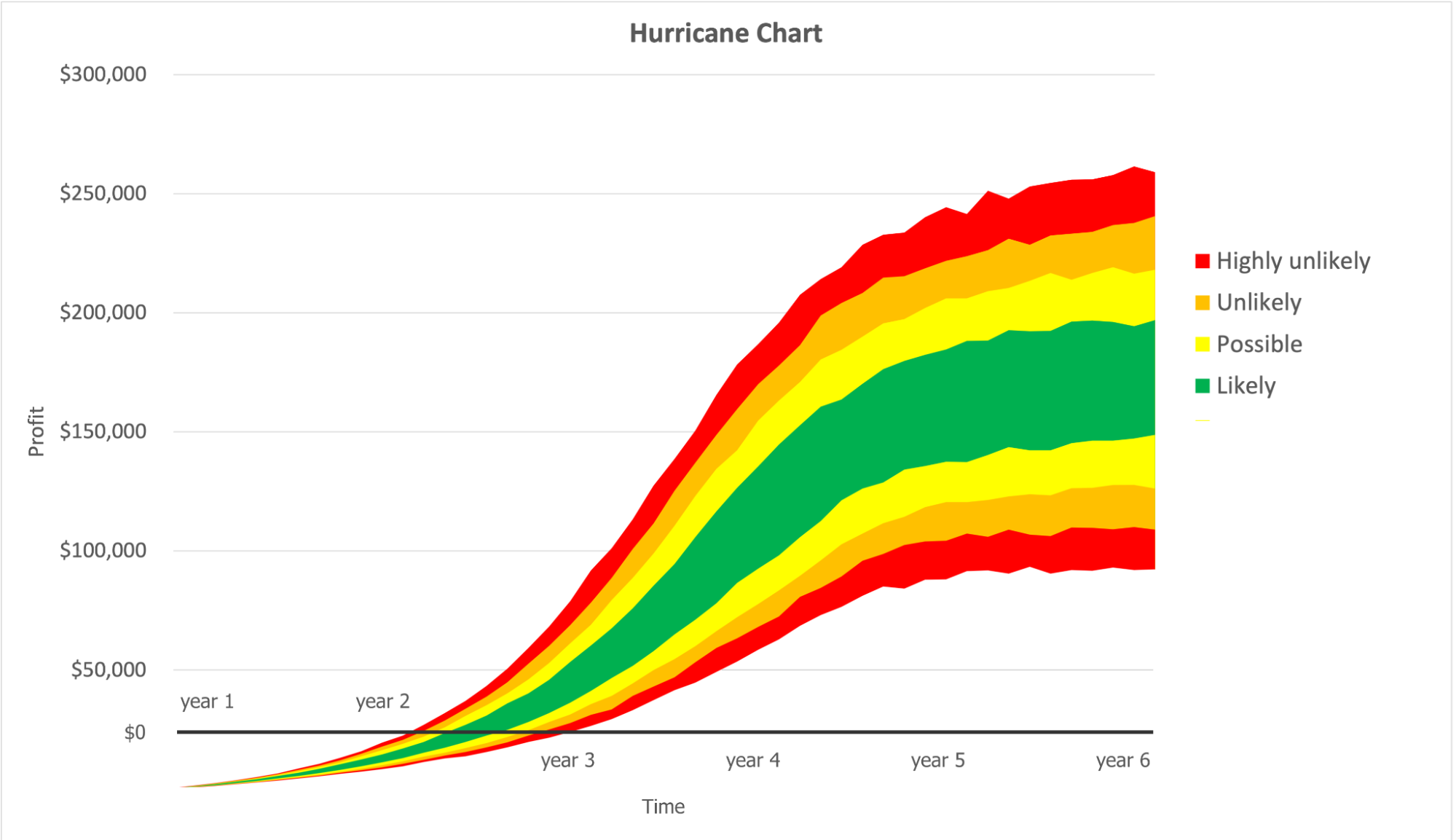

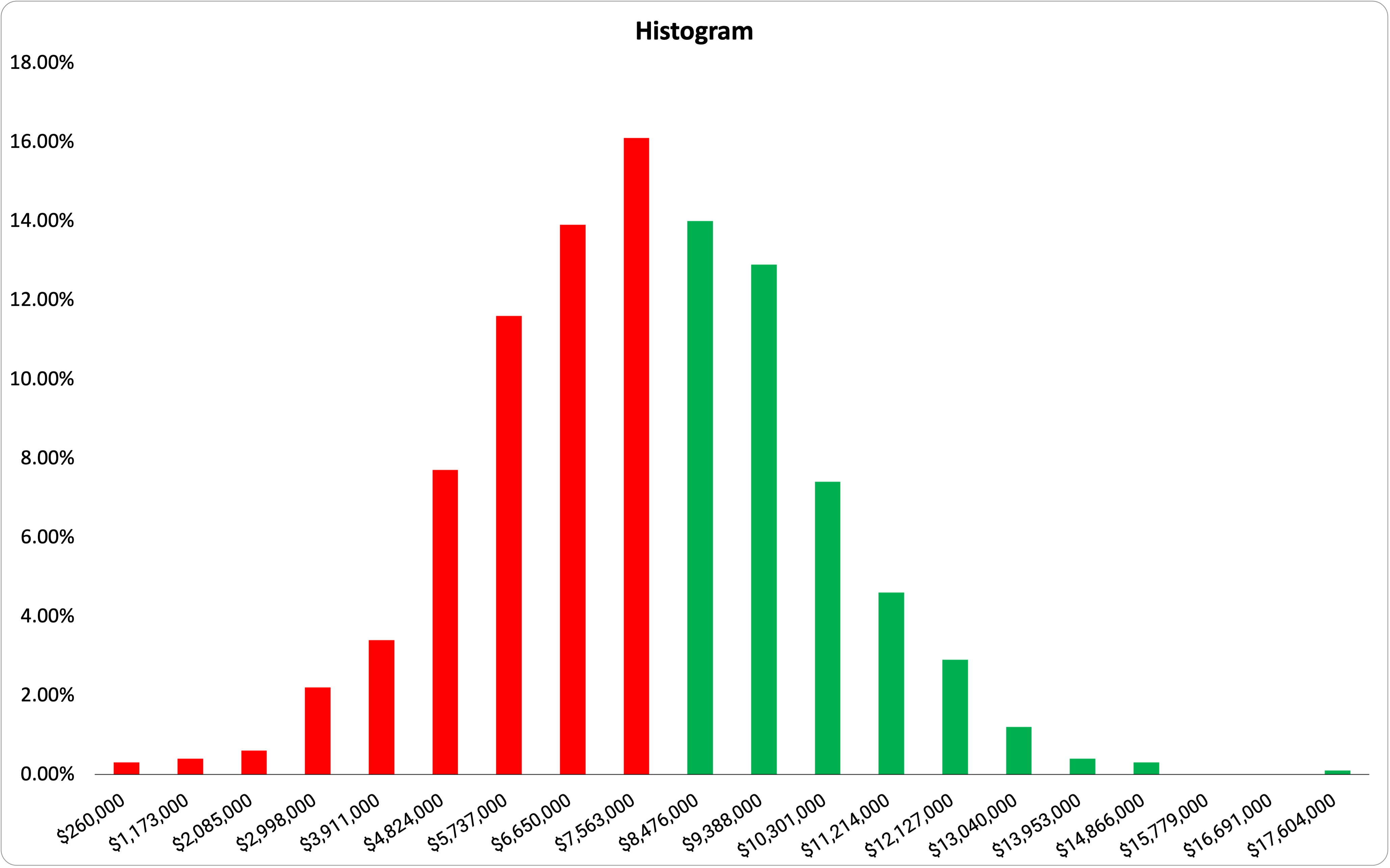

Fortunately, there is already a method to calculate the effect of uncertainty in any equation: Innovation Accounting. Innovation Accounting does not assume you know the exact value of every cash inflow and outflow or the discount rate. Instead, it allows you to represent uncertainty in your calculations using estimated ranges for every variable in a Monte Carlo simulation. In other words, it’s a way of admitting uncertainty and still using what you do know to calculate your likelihood of success. So instead of using a simple calculation that gives a single answer, we wind up with a more realistic range of possible outcomes in a hurricane graph showing how profit and loss develop over time.  You can use this exact same approach, including the Net Present Value formula, in a Monte Carlo simulation. The only difference is that since the NPV formula collapses all the cash inflows and outflows into a single number, you won’t get a hurricane graph showing what happens over time. You’ll just get a range around a single number (the NPV), which we can represent in a histogram like this:

You can use this exact same approach, including the Net Present Value formula, in a Monte Carlo simulation. The only difference is that since the NPV formula collapses all the cash inflows and outflows into a single number, you won’t get a hurricane graph showing what happens over time. You’ll just get a range around a single number (the NPV), which we can represent in a histogram like this:  We can then calculate the probability of the NPV being above or below zero to make a go/no go decision (or in lean startup methodology, a Pivot or Persevere decision.) So to finally answer the original question I just geeked out on, we do not explicitly teach how to do NPV calculations in our Innovation Accounting program (you can Google it or use Excel’s built-in functionality). Instead, we work individually with everyone in the program on their own models using any real numbers from real experiments, or create early stage estimates using uncertainty. If you want to use the Net Present Value formula, it’s very simple to integrate NPV into your Monte Carlo simulation. You just need to estimate your opportunity cost to figure out your discount rate.

We can then calculate the probability of the NPV being above or below zero to make a go/no go decision (or in lean startup methodology, a Pivot or Persevere decision.) So to finally answer the original question I just geeked out on, we do not explicitly teach how to do NPV calculations in our Innovation Accounting program (you can Google it or use Excel’s built-in functionality). Instead, we work individually with everyone in the program on their own models using any real numbers from real experiments, or create early stage estimates using uncertainty. If you want to use the Net Present Value formula, it’s very simple to integrate NPV into your Monte Carlo simulation. You just need to estimate your opportunity cost to figure out your discount rate.

Lessons Learned

- The Net Present Value formula is a way of collapsing future cash inflows and outflows into today’s value for easy comparison.

- The Net Present Value formula is not a replacement for Innovation Accounting.

- The Net Present Value formula can be used within Innovation Accounting for making Pivot-or-Persevere decisions.

Interested in understanding more about NPV? Download an example Monte Carlo simulation! Special thanks to Jon Ruark for reviewing and giving feedback on this post.

Frequently Asked Questions

What is the net present value formula and how does it work?

The net present value formula collapses a timeline of future cash inflows and outflows into a single number expressed in today’s dollars, accounting for the opportunity cost of investing your money elsewhere. If the NPV is greater than zero, the investment is worthwhile; if it’s below zero, you’d be better off putting your money into a safer alternative like a savings account.

Why shouldn’t you use NPV for innovation projects?

As product managers, we can only use the net present value formula effectively when we have high confidence in the projected cash flows and discount rate. Innovation projects are full of uncertainty — revenue in Year 4 could be $1M or $137.57. Without reliable numbers, NPV becomes a “garbage in, garbage out” calculation that dresses up assumptions to look more precise and scientific than they actually are.

How can you combine NPV with Innovation Accounting?

Instead of plugging single-point estimates into an NPV calculation, we can use estimated ranges for every variable in a Monte Carlo simulation. This produces a histogram showing the probability distribution of NPV outcomes rather than a single misleading number. We can then calculate the likelihood of NPV being above or below zero to make informed Pivot-or-Persevere decisions.

What is the discount rate in an NPV calculation?

The discount rate represents the opportunity cost of putting your money into a specific investment rather than a safer alternative. For example, if you could earn 5% interest in a savings account, that becomes your baseline discount rate. Any investment earning less than that rate would have a negative NPV, meaning you’d be better off leaving your money in the bank.

Is NPV the same as Innovation Accounting?

No. The net present value formula is not a replacement for Innovation Accounting — it’s a tool that can be integrated within it. NPV assumes you know exact future cash flows, while Innovation Accounting explicitly accounts for uncertainty by using estimated ranges and Monte Carlo simulations to produce a realistic spectrum of possible outcomes rather than a single number.

Comments

Loading comments…

Leave a comment